Hunting at the housing sector in the decades 2020-2024, a person possibility i identified early on was that house charges could speed up much more in this time period than we noticed in the earlier enlargement if stock channels broke to all-time lows.

I talked about obtaining a 23% value-advancement model for the housing market in the decades 2020-2024 as a essential marker of balanced growth versus overheating, primarily as stock experienced been falling for a long time appropriate into our critical demographic patch. Sluggish and continual normally wins, but in some cases fate deals you a terrible hand, and not significantly can be carried out when the market overrides anyone’s want for equilibrium.

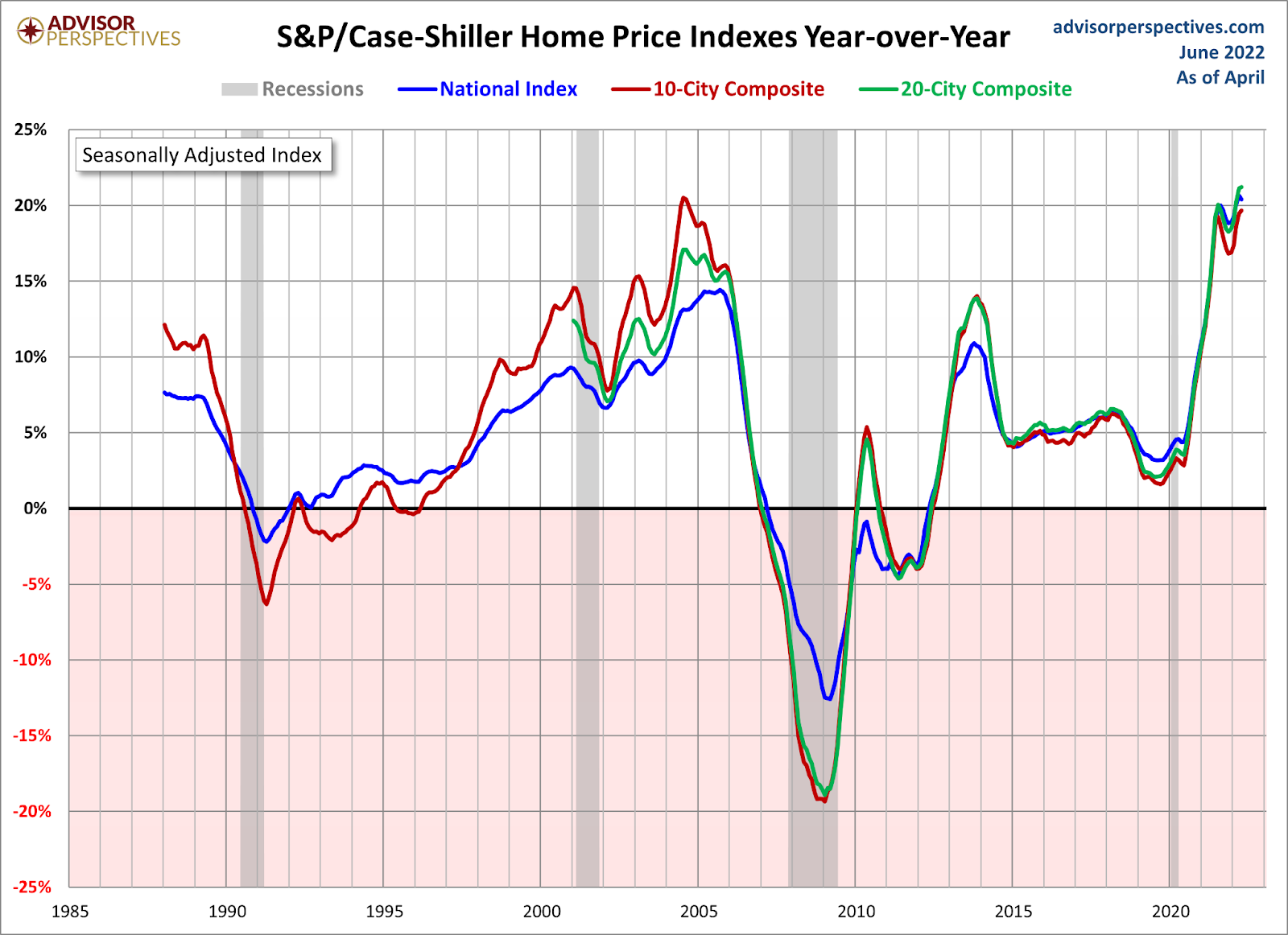

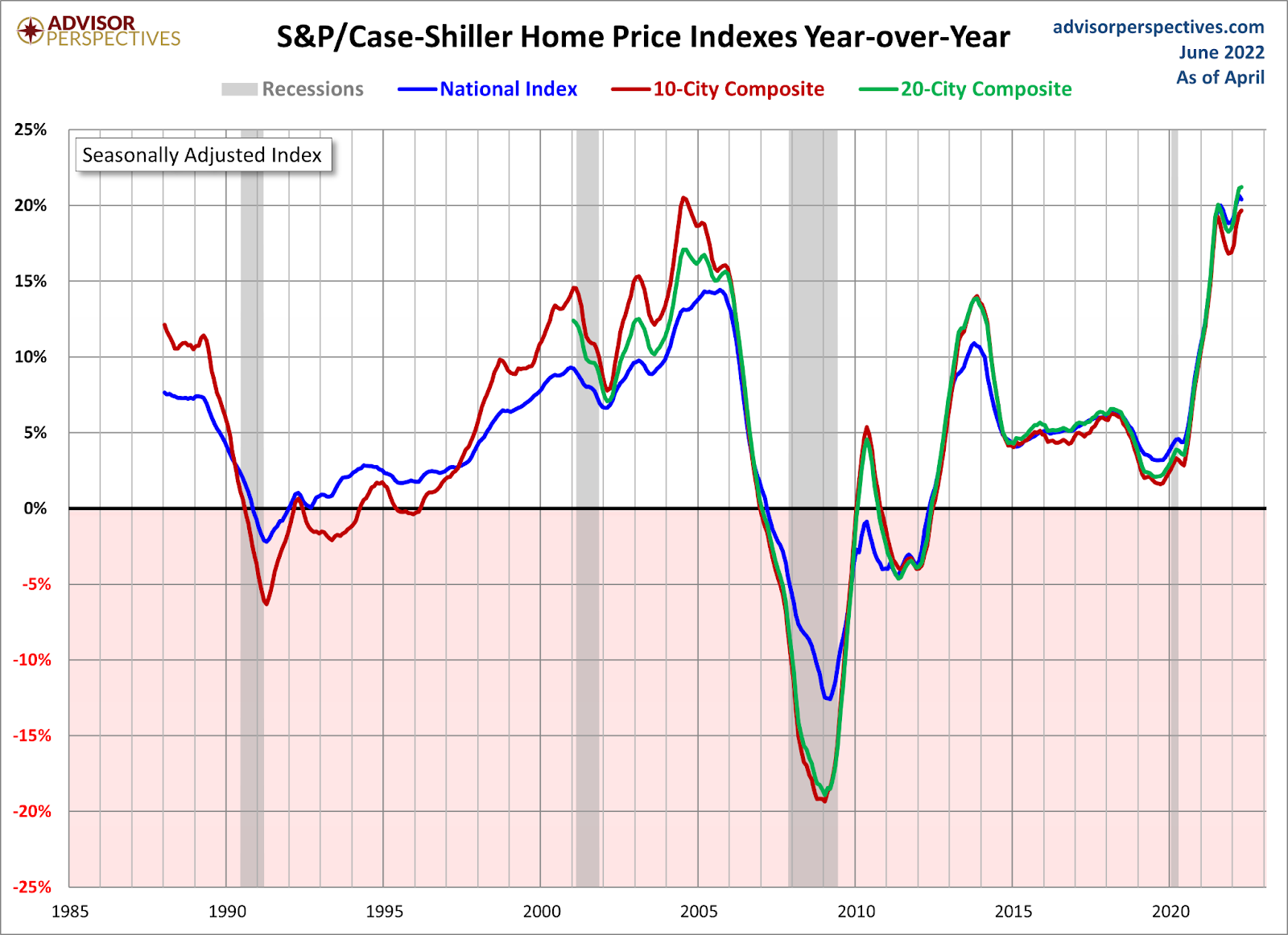

Above the very last two and a 50 % decades of U.S. housing, one particular detail that will make the history guides is that it was not housing deflation we essential to worry about, but housing inflation on each ends: household prices and rents.

Immediately after 2021 finished and my cost-advancement model was damaged right after only two years and we begun 2022 at all-time lows in inventory, I labeled the U.S. housing industry as savagely unhealthy. This challenge is considerably distinctive than the housing credit bubble of 2002-2005. Back again then, we had higher gross sales, bigger stock, and much less cost development, but we experienced a huge credit rating bubble. Today we have much less profits, few listings, and considerably hotter residence-price tag expansion.

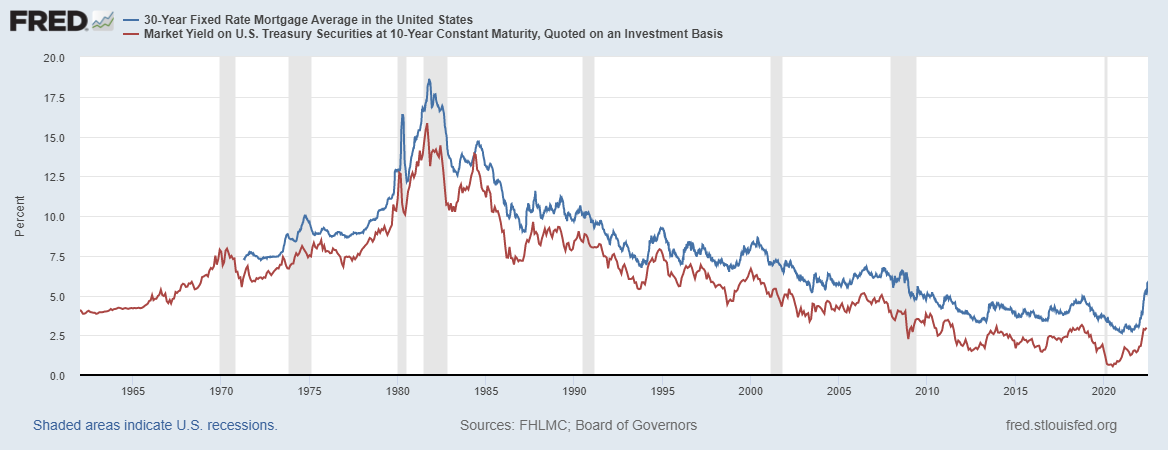

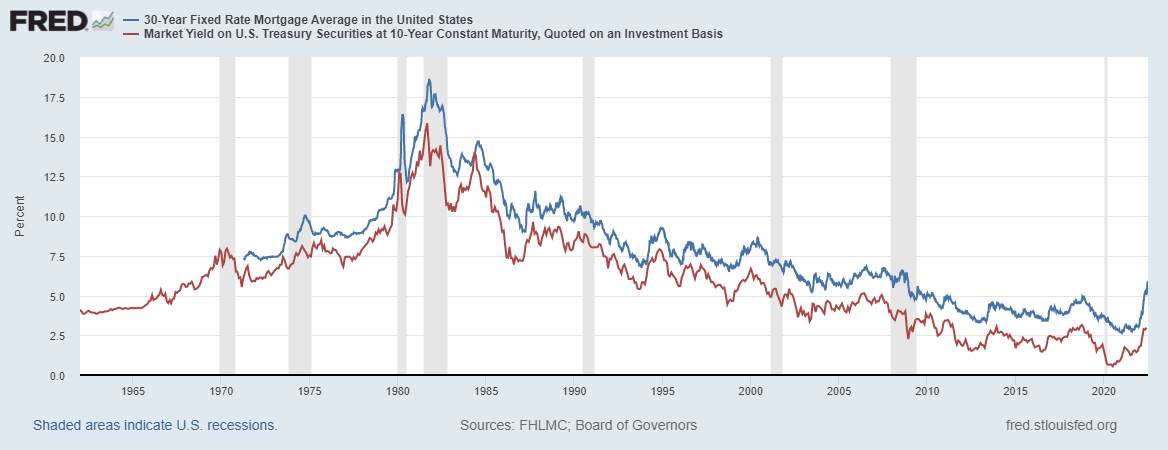

When I talked about needing increased rates in February of 2021, it was based on the reality that we did not have a credit bubble, so the demand from customers is legit. However, this also implies that demand has limits. The reality was that global bond yields have been nevertheless very low, and finding the U.S. 10-yr generate over 1.94% was heading to be problematic. As inventory fell yet again, bidding wars grew to become the norm, and property costs escalated.

By October of 2021, it was obvious that stock had no probability of displaying any 12 months-around-year progress, and we have been heading to an even even worse home-rate development inflation story in 2022 unless charges rose. January and February data appeared so lousy that I threw in the towel and reported nothing at all else matters at this stage — we need to have rates to rise to consider to awesome this sector down.

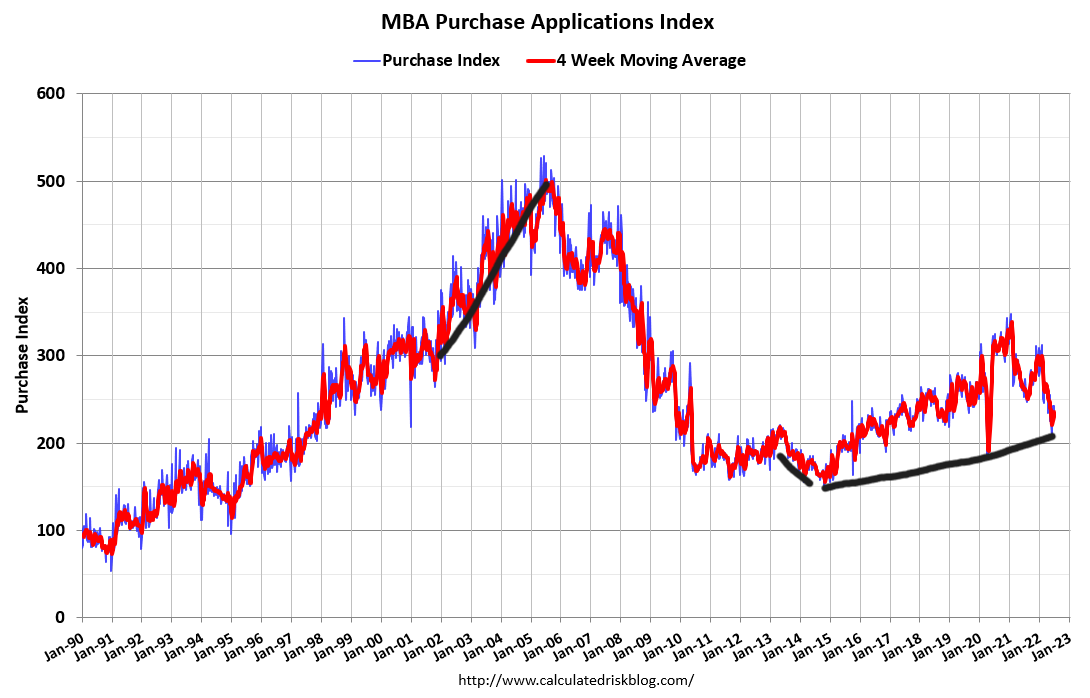

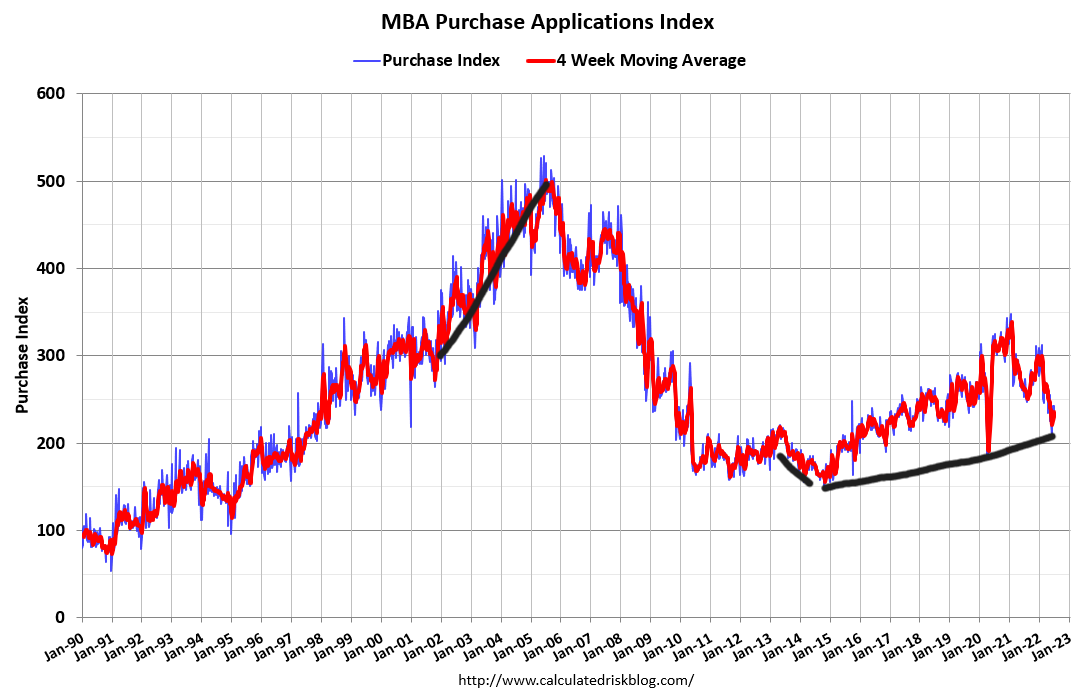

Mortgage loan prices of 4%-5% weren’t undertaking the amount of money of demand destruction I assumed they would. I was anticipating 4-week going normal year-around-12 months declines of 18%-22%, but we were being seeing high single-digit and decrease double-digit declines. Home finance loan fees nearer to 6% for confident are driving bigger calendar year-about-12 months decline knowledge. Even now, I never received the four-week shifting normal drop of 18%-22% development that I was searching for and it is now previous the conventional seasonality time for this facts line.

On Wednesday, the acquire software information was down 4% 7 days to week, 18% year more than calendar year, and the four-week going average decrease is now down 17.25%. I will presume that the progress in ARM financial loans this yr prevented the 18%-22% yr-in excess of-year decline tendencies I was wanting for earlier in the calendar year.

By October of this yr, the 12 months-above-12 months comps will be a great deal more durable, so we can count on even bigger declines if the trend stays the very same.

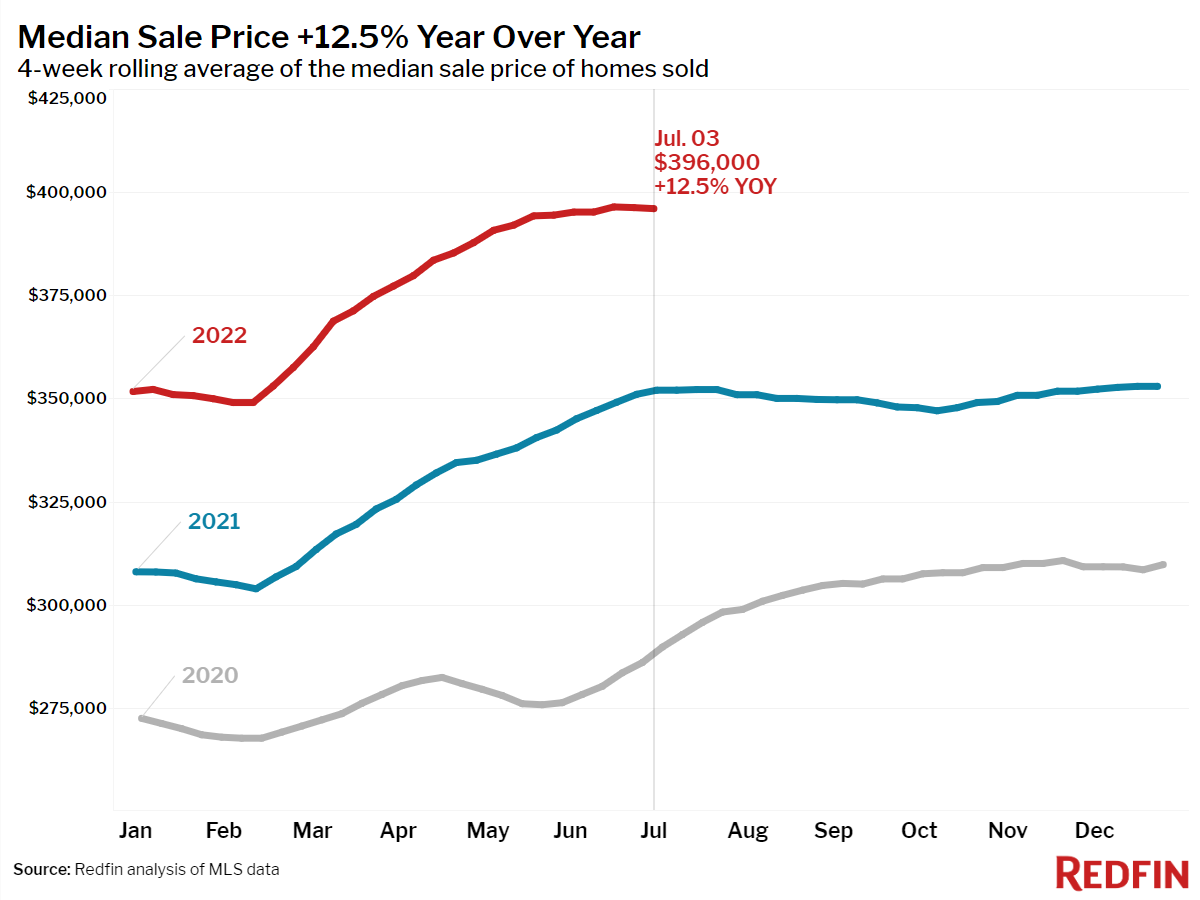

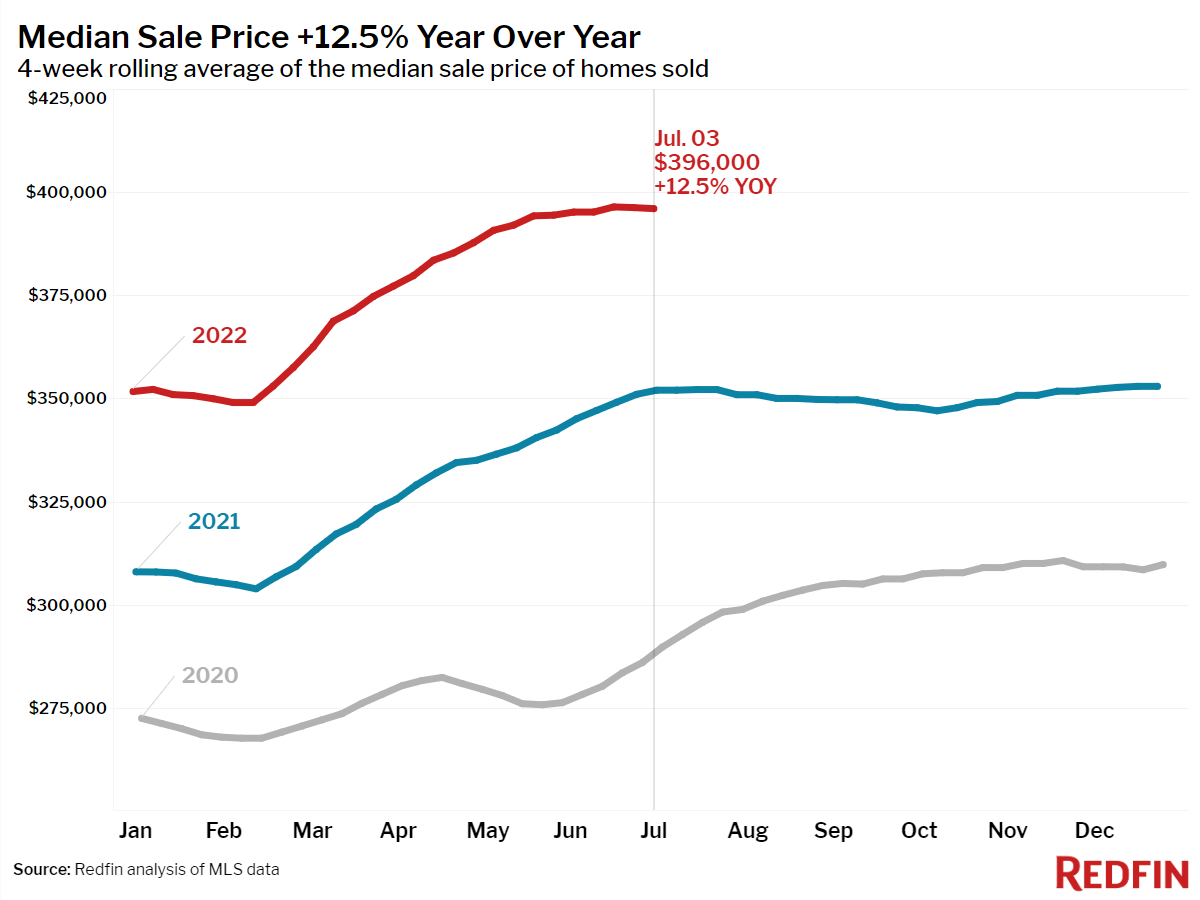

Even so, home loan fees acquiring to 6.25% in fact have picked up the speed on the 12 months-above-calendar year declines share sensible in the purchase application information. However, here are just a handful of illustrations of why we needed rates to increase. (This is not typical, individuals. You do not see percentage declines like this with calendar year-in excess of-12 months rate growth in June.)

- Las Vegas house profits were being down 24% yr in excess of yr as median product sales selling price was up 21% 12 months above calendar year.

- Orange County, California connected households in June, product sales were down 27.2%, and costs up 17.8%.

Now just think about how sizzling residence charges would be if property finance loan fees didn’t rise earlier 6% this calendar year and we didn’t consider the large strike to affordability? The housing industry always sees greater demand from customers when the 10-12 months breaks beneath 2% and we have sub-4% premiums.

In the center of the drama of larger prices, my bigger concern is in fact if costs go down once more. Dwelling sellers and builders experienced as well a lot pricing electric power, pushing charges to the extreme. My five-12 months advancement value design obtained smashed in two decades, and factors worsened in 2022 before fees rose.

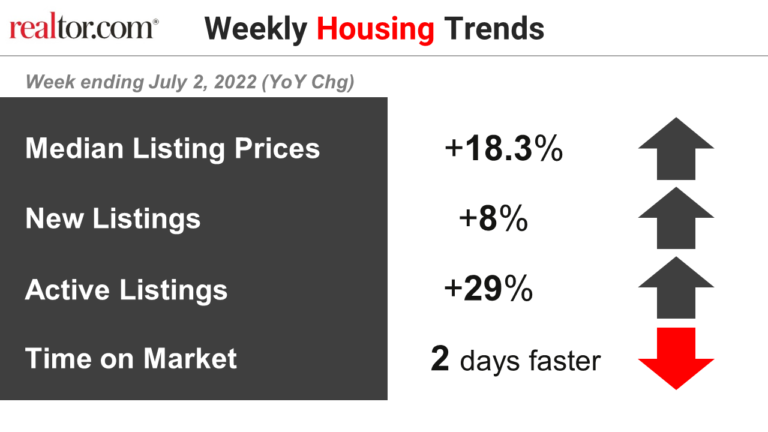

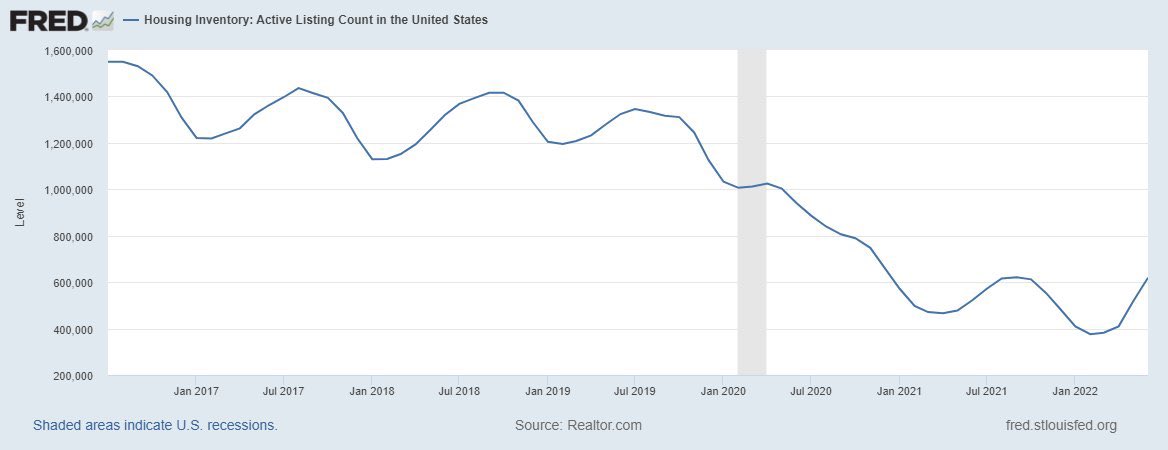

Remember, we all want a balanced housing marketplace it is a excellent detail, not negative. So the purpose for me currently is to see total stock get back to 2019 ranges. That will be positive, and we are doing the job our way there, we just require extra time due to the fact the housing marketplace of 2022 is not the pressured credit promoting housing market of 2008. I really do not need the housing industry to have 2012, 2014, orr 2016 stock amounts to be well balanced — I just will need 2019 inventory details, which is among 1.52-1.93 million households, employing the NAR details.

NAR: Complete Stock

Realtor.com and other folks have info strains that use other stock metrics. Having said that, they all pattern the exact same way.

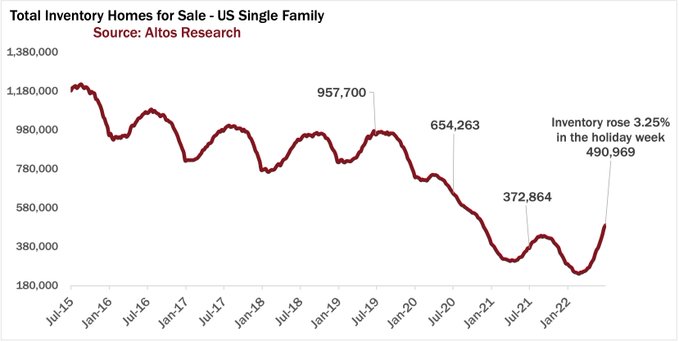

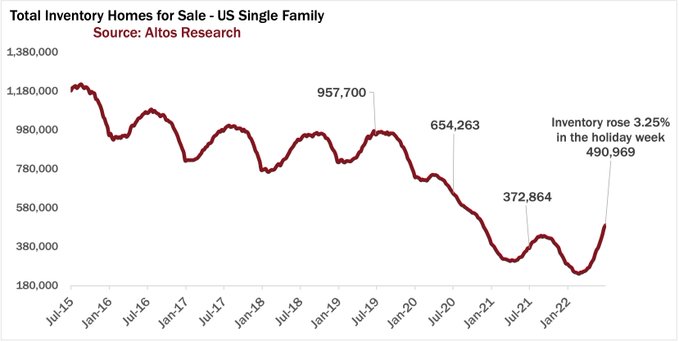

From Altos Investigate:

I a short while ago did a podcast with Mike Simonsen from Altos Exploration on this matter.

As the economic cycle shows much more recessionary data strains, historically, the bond sector and home loan rates head down together.

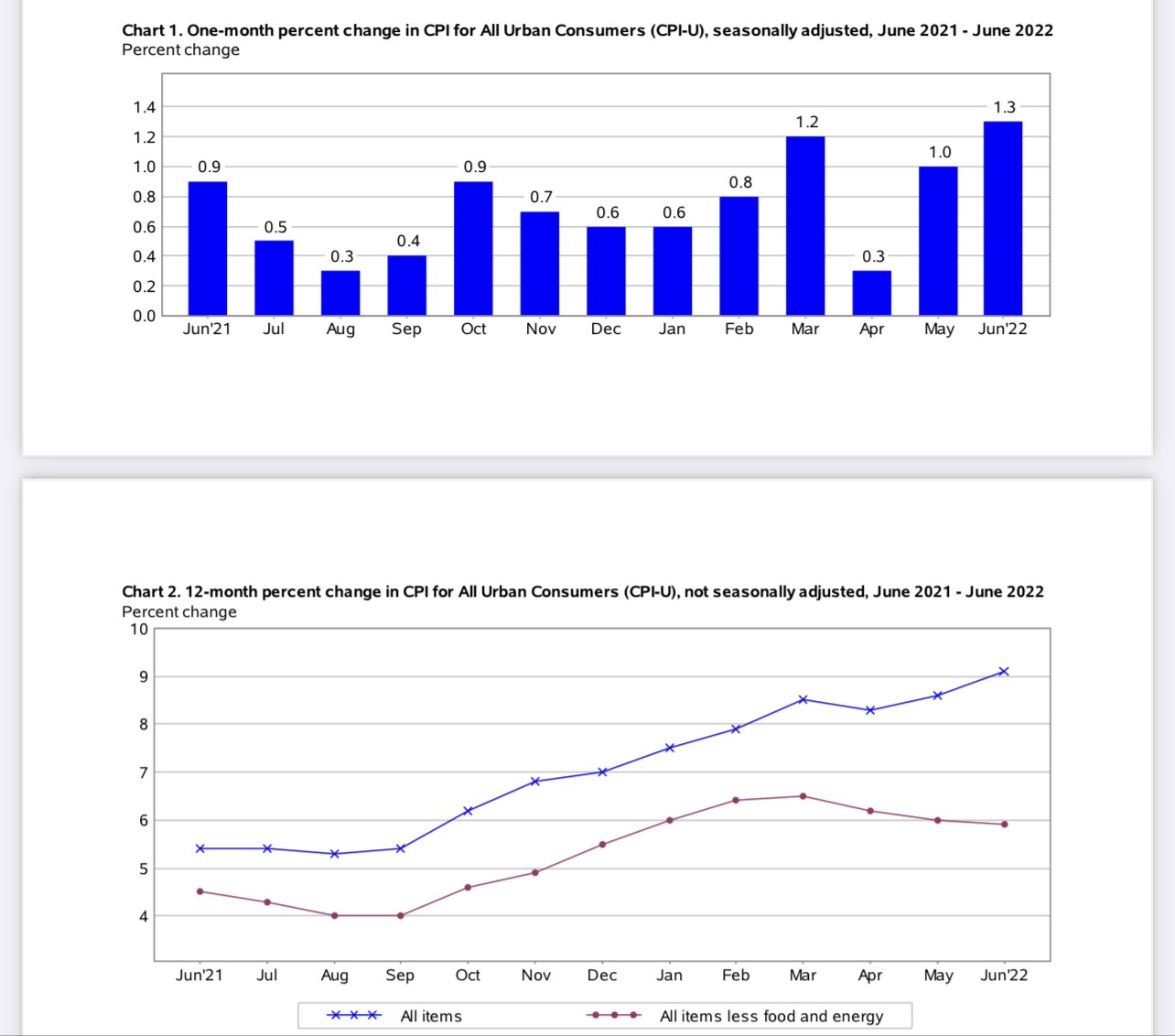

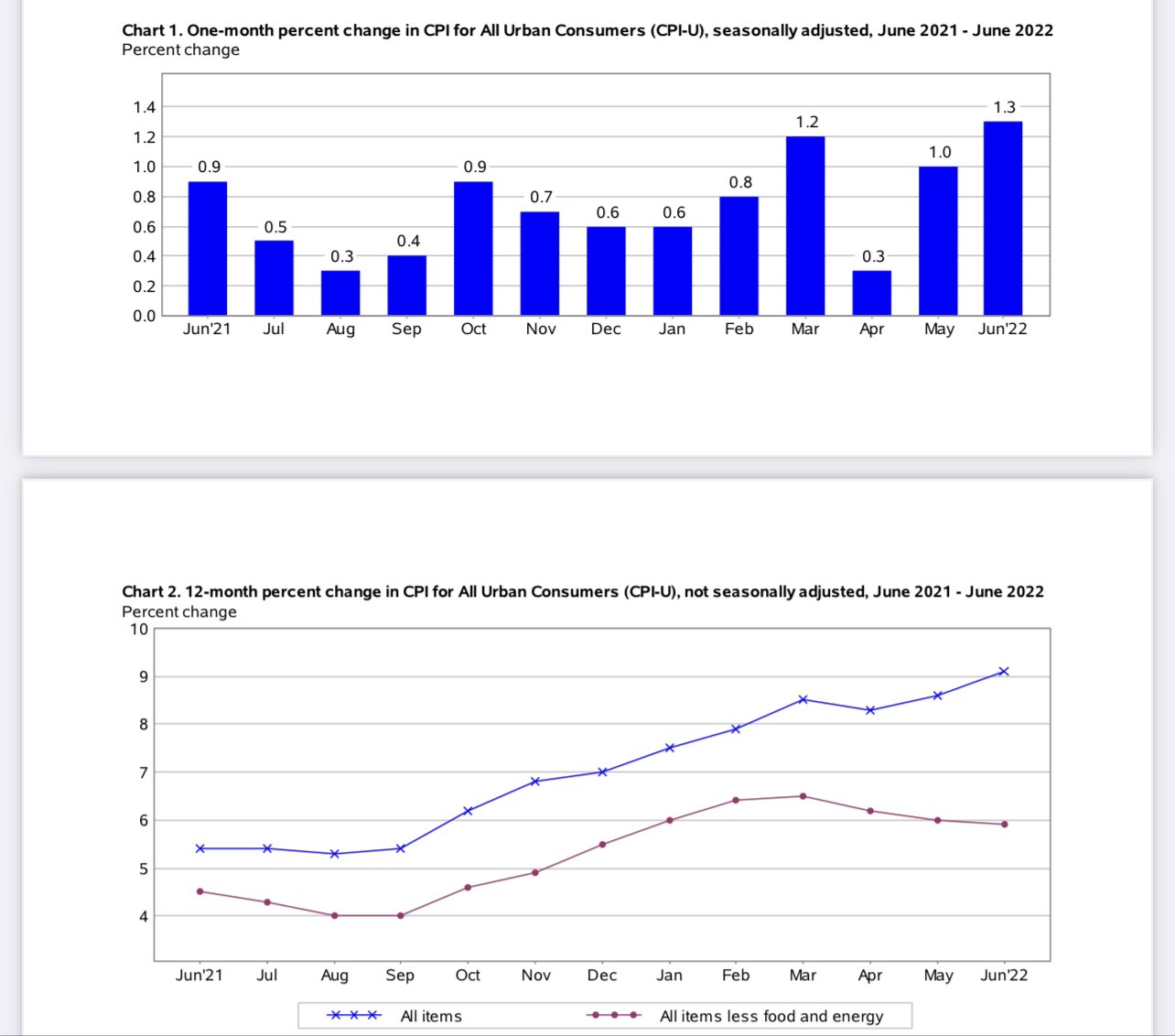

On Wednesday we had a further sizzling CPI print, and the 10-calendar year yield is buying and selling at 2.93%. This is not even the superior we had back in 2018 when inflation expansion was cooler. Quite a few people today feel home finance loan costs should be greater currently if they were tracking the expansion price of inflation, that means bond yields should really be a great deal larger, way too. Nevertheless, since 2021, bond yields haven’t adopted the progress amount of inflation.

From BLS:

The downside of better fees

Housing construction will slow

Keeping in line with my summertime of 2020 premise that for the sector to change, it requires a 10-yr generate previously mentioned 1.94% and with duration to effect income negatively. The new house gross sales sector will gradual down like it often does. Even in March of this year, when the knowledge wasn’t terrible, the market was at chance.

Just final month, I elevated my fifth economic downturn red flag, figuring out that the builders were being at the level of pulling back again on construction and concentrating on offering what households they experienced still left and dealing with cancelation premiums rising. My just one argument below is that if we require 3%-4% mortgage loan costs for the builders to make at the expense of house prices rising 15%-20% a calendar year, it’s not a good trade off.

Employment and incomes will be lost.

As we all know, we have several organizations in the real estate and home loan sector that are laying off people. It isn’t just the companies that boomed due to COVID-19, so we have genuine-daily life product hurt to households. Also, with fewer transactions occurring, considerably less transfer of commission will take place in housing.

Acquiring nearer to a economic downturn

With the fifth economic downturn crimson flag raised thanks to greater home finance loan fees, we are receiving closer and nearer to a total economic downturn in the U.S., which in aspect means a lot more Americans are getting rid of their careers and life remaining turned upside down. With bigger charges, inflation, and no work, it is a stressful time for any household, especially these with youngsters.

To wrap up, I labeled this current market savagely unhealthy before this year due to the fact I knew what this knowledge would glance like. House rates are increasing even with larger costs, so we aren’t benefiting from falling household price ranges, even even though income are dropping. This has occurred just before when charges rose, revenue fall, and value advancement would great down but not go damaging.

Nonetheless, it is a various ball video game listed here in 2020-2024. The S&P CoreLogic Situation Shiller Property Price Index, while it lags, however shows 20% furthermore yr-in excess of-calendar year development. In the past, with increased costs, the progress rate would cool down towards one digits. Evidently, we aren’t there still, but we really should be receiving there in time with the mounting stock.

With any luck ,, this explains why I am portion of “team bigger rates” and why I believe a balanced housing sector is the greatest. Larger prices are performing it just can take more time to get us back again to 2019 levels of inventory.

More Stories

Auction Home Closing Process Explained Simply

Are Dubai Villas the Ultimate Real Estate Investment?

Due Diligence in Commercial Real Estate Transactions